フランシスコ教皇の言うperipheral labor, labor peripheralsとは何か、調べていったところこの論文集:Peripheral Labour: Studies in the History of Partial Proletarianization (International Review of Social History Supplements, Series Number 4) Cambridge University Press, 2008年、にあたった。文章を幾つか半訳しておく。

フランシスコ教皇の言うperipheral labor, labor peripheralsとは何か、調べていったところこの論文集:Peripheral Labour: Studies in the History of Partial Proletarianization (International Review of Social History Supplements, Series Number 4) Cambridge University Press, 2008年、にあたった。文章を幾つか半訳しておく。

1)本のdescription:

This volume takes an alternative look at the notion of ‘wage-workers’. The contributors suggest that the idea of a ‘pure’ working class should be reconsidered and examine specific South Asian and Latin American case studies. A large part of the working class in the so-called third world and also in the main capitalist countries is either free (but coerced through non-economic means) or does hidden work labor e.g. as formally self-employed producers. By rethinking the fundamental assumptions of ‘classical’ labor and working-class history, the volume contributes to the development of a non-Eurocentric historiography.

本書は’wage-workers’概念について旧来定義に代わる見方を採用する。本著者達は、「純粋」労働者階級というアイデアは再考されなければならないと考え、南アジアと中南米(Latin America)について幾つかの特定case studiesを行った。所謂第三世界において、また主要資本主義諸国においても、大部分の労働者階級は、free(ただし、非経済的手段によって強制されている)か、あるいは、例えば形式的な個人事業主としてhidden work laborを行っているか、のどちらかである。「古典的」laborおよび労働者階級の歴史という基本前提を再考することによって、非ヨーロッパ中心主義的な歴史科学の論理展開に、本書は貢献している。

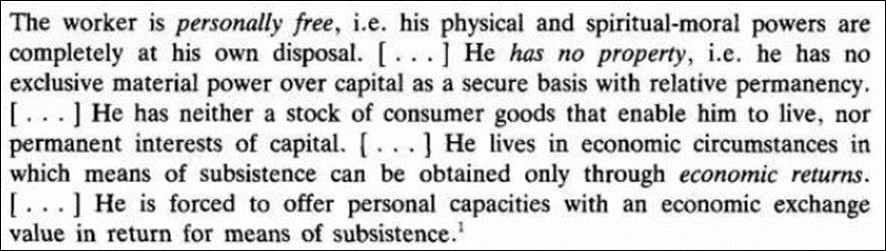

2)本書1page、wage labourersの定義、Goetz Briefs(1889-1974。カトリック社会神学者。教皇ピオ11世1931年回勅Quadragesimo annoの基本思想を提供)による。:

a wage labourerはpersonally free、即ち、彼の形而下的およびspiritualなmoral powersは完全に彼自身の意のままにすることができる。中略。しかしながら彼はno property、即ち、資本に対抗できるexclusive material powerを、相対的恒常性のある安定基本財として持っていない。中略。彼は、生きていくための消費財ストックも、恒常的な資本利潤も、持っていない。中略。彼は、必要最低限の生活手段をeconomic returnsからのみ獲得するという経済環境の中で生きている。中略。彼は、必要最低限の生活手段を得るために、自らのpersonal capacitiesを経済的価値交換に供するよう強いられている。

3)本書とは別だが、教皇が多用するperipheryについて短く解説した文章を見つけた。

”The Concept of Periphery in Pope Francis’ Discourse” Abstract:

Since the beginning of his mandate, Pope Francis has used the concept of periphery as a metaphor of social marginality. However, the notion of periphery also seems to target the asymmetries generated by the liberal version of globalization. Pope Francis’ narrative has to be read in the broader context of the relation between religions and globalization. That interaction is usually conceptualized in terms of religions capitalizing on global “vectors”, such as new information and communication technologies, processes of political and institutional integration, shared cultural patterns, transnational phenomena and organizations. An alternative way to analyze the role of religions consists in considering them as agencies defending the perspective of a universal community, putting into question the national political boundaries and contesting the existing global order. Understood in those terms, the concept of periphery reveals to be a powerful rhetoric device, insofar as it suggests that it is possible to get a wider perspective of the current state of the world looking form the edge rather than from the center.

「フランシスコ教皇の言説に現れるperipheryコンセプトについて」アブストラクト:

フランシスコ教皇は教導開始以来、periphery(辺境、周辺)というコンセプトを、社会辺境部のたとえとして使い続けている。更に言えばperipheryという概念の矛先を、the liberal version of globalizationによって生じる非対称性に向けているようである。フランシスコ教皇の話す物語は、religionsとglobalizationとの相互関係性という広い文脈において読み解かれる必要がある。この相互関係性は通常、religionsの持つglobal “vectors”(訳註:全方位性)という利点を活用する、という観点から概念化される。それは例えば、新たな情報通信技術、政治的・制度的な高次統合プロセス、共有化される文化パターン、脱国家的な現象および有機組織体、などである。religionsのこういった役目を分析するには従来とは代わった方法が必要である。それはreligionsを、普遍共同体の視点を防衛し、政治的国境に疑問符をつけ、既存の世界秩序に反論を投げかける、agenciesと見なすというものである。この様に理解すれば、periphery(辺境、周辺)というコンセプトは、この形而下地上世界の現状を中心から見るよりも辺縁から見た方が比較的広く展望できると示唆される限りにおいて、a powerful rhetoric deviceとなって立ち現れるのである。

現行経済は、ある程度楽しかったかもしれない。でも、その百倍いや千倍楽しい新たな経済が、確かにある。

現行経済は、ある程度楽しかったかもしれない。でも、その百倍いや千倍楽しい新たな経済が、確かにある。